Retirement looms around the corner, and knowing if you have enough saved can be a bit overwhelming. Credit card debt, student loans, and inconsistent income all play a major role in savings goals. But having a clear picture of where your savings should be can help alleviate the pressure of where you are financially. In this article, we'll break down how much the average American has saved, what experts recommend saving by age, and why many people fall short. You'll learn how to catch up if you're behind, why Gen Z is saving earlier than ever, how new policies like SECURE 2.0 are shifting the landscape, and how tools like Cheers Credit Builder can help you grow your credit and savings at the same time. Whether you're starting in the workforce or retirement is right around the corner, this guide can help show you some figures to help you stay on track.

What the Average American Has Saved by Age

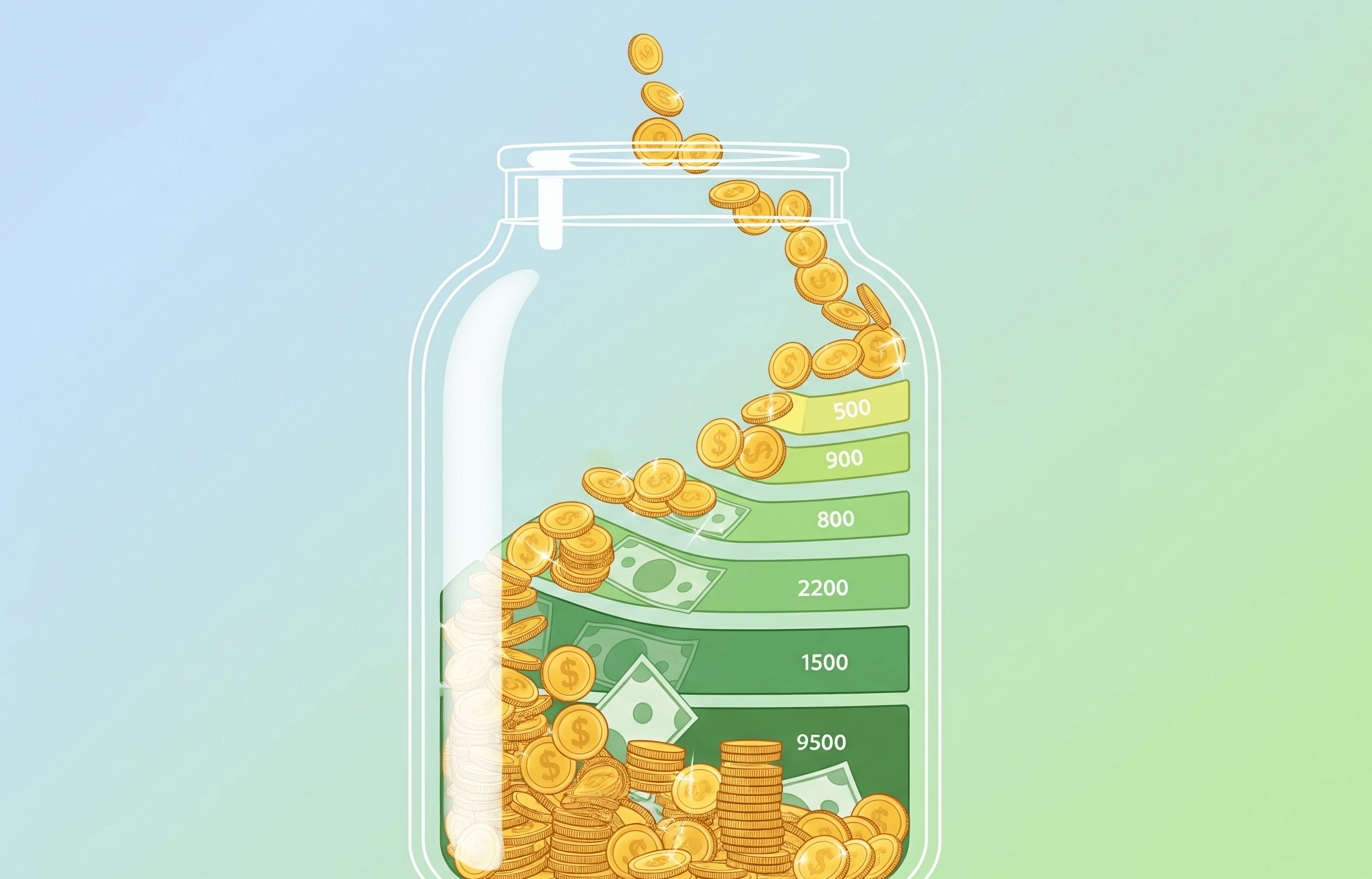

A 2024 study showed how Americans' retirement savings stack up by age group:

- Ages 25-34: $30,017

- Ages 35-44: $76,354

- Ages 45-54: $115,703

- Ages 55-64: $204,022

- Age 65+: $232,710

These numbers highlight a common gap between what people have saved and what they might need. The earlier you understand that gap, the more time you have to close it.

Recommended Retirement Savings by Age

Financial institutions like Fidelity and T. Rowe Price recommend saving based on your income, rather than an arbitrary number. Their general rule of thumb is to save your entire salary by the age of 30. Then 3 times your salary at 40, 6 times at 50, and ideally, 8 times by 60 years old. At around 67 or retirement age, it's ideal to save 10 times your salary. So, if you're earning $70,000, the recommendation is to have $ 70,000 saved by 30, $ 210,000 by 40, and so on. These benchmarks adjust for your income over time, helping you focus on progress rather than perfection.

Why the Gap Exists: Inflation, Wages, and Late Starts

Many people are behind on their retirement savings, not because they're careless, but due to real financial pressures. Wages haven't kept pace with inflation, housing costs are high, and younger workers often face student loan debt immediately after college. Not everyone has access to a workplace retirement plan, and gig workers or entrepreneurs are usually left to figure it out on their own. For some, retirement feels like something to worry about later, but that delay makes catching up even harder. The good news? Policy shifts and savings tools are making it easier to course-correct, even if you got a late start.

2025 Retirement Trends to Watch

Gen Z Is Getting a Head Start

Thanks to auto-enrollment and increased financial awareness, Gen Z is saving earlier than previous generations. Many people join 401(k) plans by the time they are 22. That head start compounds over time, giving them an advantage most Millennials didn't have.

The Catch-Up Era Begins at 60

Under the SECURE 2.0 Act, starting in 2025, workers aged 60-63 can contribute even more to retirement accounts, up to 150% of the standard catch-up limit. That's a big deal for Gen Xers who feel behind and want to boost savings in their final working years.

Crypto & Alternative Investments Enter the Picture

New proposals allow 401(k) providers to offer cryptocurrencies, gold, and private equity funds. While these can offer growth potential, they're also volatile. These alternatives should be used cautiously and never replace a core retirement strategy.

The "Fragile Decade" Anxiety

Many Americans in their 40s and 50s feel like they're too late. A recent study found that nearly half of the people in their prime earning years worry about retirement daily. But even small, consistent increases in savings, especially with tax-advantaged accounts, can help close the gap.

What You Can Do Right Now

Regardless of age, you can always prioritize your savings goals, and you will thank yourself for doing so. If you're in your 20s or 30s, start small and automate your contributions, whether to a Roth IRA or a workplace 401(k). Ensure you're taking advantage of any employer match, and avoid touching your retirement savings when you change jobs. In your 40s and 50s, check how your savings compare to the recommended salary multiples and increase your contributions if you can. Take advantage of catch-up contributions if you're over 50 years old. Those in their 60s should focus on protecting what they've built, reviewing investment risk, and planning the right time to claim Social Security. Each decade brings different challenges, but the earlier you start, the more options you'll have.

How Cheers Helps You Build Credit While Saving

If you're trying to boost your retirement savings but your credit score is holding you back, Cheers Credit Builder offers a smart way to make progress on both fronts. It works by setting up a savings-based installment loan, no hard credit check required. You pick a plan, make monthly payments, and Cheers reports those payments to all three credit bureaus. Over time, this helps build a positive payment history, which can influence up to 35% of your credit score. At the end of the loan term, you get your payments back (minus interest), making it a practical way to improve your credit while growing your savings. With flexible terms, no membership or setup fees, and fast credit reporting, Cheers helps you move toward financial milestones faster, including retirement.

Cheers is not a bank—deposit account held by Sunrise Bank, Member FDIC.

Final Thought: It's Not Too Late to Start

Regardless of your current age, the most crucial step is the next one. Starting with a single automatic deposit, opening an IRA, or improving your credit with a tool like Cheers-all of it counts.

The recommended retirement savings by age benchmarks are just guideposts. Life happens. However, with consistency, the right tools, and a little help along the way, building a secure retirement remains within reach.