If you've been wondering, "Does opening a savings account affect credit score?", you're not alone, and the answer is more straightforward than it seems. Opening a savings account doesn't directly affect your credit score. It won't appear on your credit report, and in most cases, no credit check is involved at all. But that's not the end of the story. There are still indirect connections between saving and credit, particularly in terms of overdraft features, identity checks, and how savings can help prevent credit-damaging behaviors. In this article, we'll explore the different ways savings accounts and credit health overlap, explain what banks check during the process, and show you how to take control of your credit journey, whether you're just getting started or rebuilding from scratch.

What Affects Your Credit Score (And What Doesn't)

Credit scores are built on how well you manage borrowed money, not where you store your cash. This includes information such as credit cards, loans, and payment history. Since a savings account isn't a form of credit, it doesn't get reported to the credit bureaus. That means the answer to whether opening a savings account affects credit score is a simple no, at least in direct terms.

Why Some People Think It Does

This question keeps popping up because certain banking activities can be tied to your credit report, just not savings alone. In most cases, when you open a savings account, the bank performs a soft inquiry, which is a background check that doesn't impact your score. However, there are exceptions. If you opt into overdraft protection that's connected to a credit line or link your savings to a credit-based product, the bank may run a hard inquiry. These inquiries do impact your score slightly, usually by a few points. But again, the average savings account setup doesn't include this. Does opening a savings account affect your credit score? Under normal circumstances, it doesn't.

ChexSystems and Banking History

To answer: "Does opening a savings account affect credit score?" from another angle, let's talk about ChexSystems. This isn't a credit bureau-it's a reporting system that tracks your banking behavior. If you've ever had an account closed due to overdrafts or unpaid fees, that history might appear in your ChexSystems file.

While ChexSystems reports can prevent you from opening a new bank account, they don't influence your credit score. That said, if a bank reviews your ChexSystems report and sees red flags, it may deny your savings account application. It's a separate system, but one that still matters if you're trying to take steps toward financial stability.

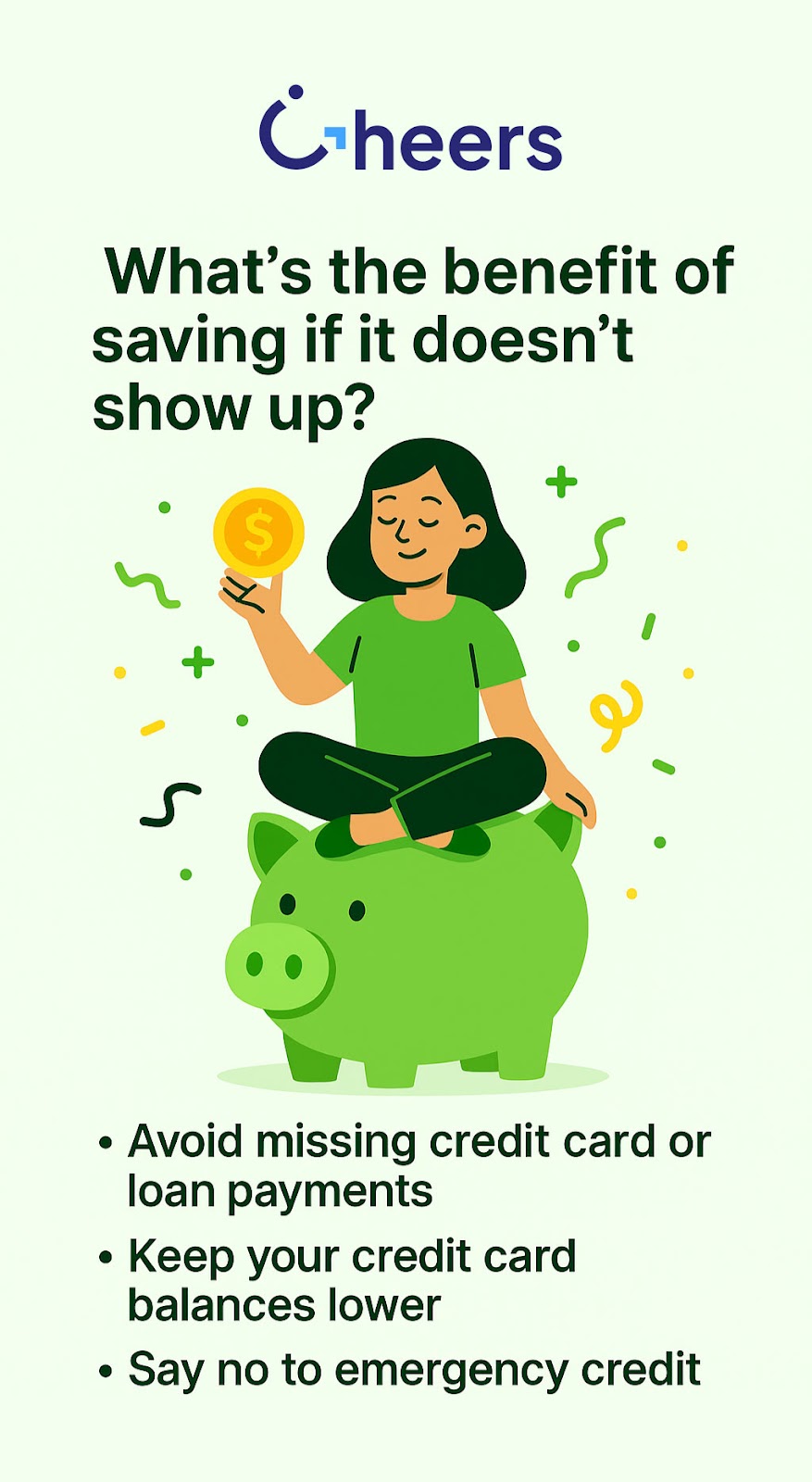

So, What's the Benefit of Saving If It Doesn't Show Up?

Just because the answer to "Does opening a savings account affect credit score?" is "no," doesn't mean savings aren't part of a smart credit strategy. A savings account gives you a financial cushion. That cushion helps you:

- Avoid missing credit card or loan payments when life gets expensive

- Keep your credit card balances lower, which improves your credit utilization

- Say no to payday loans or emergency credit use

These are all credit-positive behaviors. So while savings won't show up in your credit file, it supports the habits that do raise your score.

More Savings Accounts, Same Credit Impact (Zero)

With interest rates rising, more people are opening high-yield savings accounts to maximize their returns on their money. Some are even using multiple accounts to separate goals, such as travel, emergencies, or car repairs. Does opening a savings account affect your credit score when you open more than one? Don't worry. The answer stays the same. There's no penalty for having more than one savings account, and each one can help keep your money organized without touching your credit.

Building Credit on Purpose, Not by Accident

If you're trying to improve your credit, a savings account by itself won't be enough. However, pairing savings with a dedicated credit-building tool can be a game-changer. That's where Cheers Credit Builder fits in.

Cheers is not a traditional loan. You won't face a hard credit check, and there are no admin or membership fees. You choose a repayment plan that fits your budget and start making small monthly payments. Each on-time payment is reported to all three credit bureaus, helping build a positive payment history. At the end of the term, you get your payments back (minus the 1% monthly interest), so you're saving while you build.

It's a direct answer to the limitations of savings accounts when it comes to credit building. So, if someone asks you, 'Does opening a savings account affect my credit score?' you can say no, but building credit while saving is possible with the right tools.

Cheers is not a bank—deposit accounts held by a partner bank, Member FDIC.

What to Look Out for Before Opening a Savings Account

Even though does opening a savings account affect credit score usually has a "no" answer, it's still worth asking a few questions when you apply:

- Will the bank do a hard credit check?

- Are there monthly fees or balance requirements?

- Is overdraft protection tied to a credit line (and does that trigger a credit inquiry)?

- Is the account FDIC-insured?

Being proactive helps you avoid any small risks to your credit while choosing an account that supports your savings goals.

So, Does Opening a Savings Account Affect Credit Score?

To recap: no, it doesn't. Opening a savings account won't add to your credit history, won't be reported to the credit bureaus, and won't hurt your score unless it's tied to something credit-based like a loan or overdraft line. Even then, the impact is minor and temporary. But the bigger story here is that savings still play a decisive role. They give you control. They keep your financial life flexible. And they make it easier to use credit responsibly.

If you're looking to go beyond saving and build credit, Cheers Credit Builder gives you a way to do both-save money and strengthen your score at the same time.