If you've ever looked at your bank account and wondered, Am I where I should be?-you're not alone. The question of how much I should have in savings is one that most people ask at some point. The answer isn't one-size-fits-all, but there are benchmarks, strategies, and tools that can help. This guide breaks down how to calculate your ideal emergency fund, how your savings goals should evolve, what current trends are saying (spoiler: 3-6 months may not be enough anymore), and how savings goals shift depending on your age and income. We'll also cover what to do if saving feels out of reach right now, how to grow your savings once you've met your first goal, and how you can build your credit while you save. Whether you're just getting started or rethinking your strategy, this article is designed to help you move forward with confidence.

When the Future Feels Uncertain, Cash Creates Confidence

Let's face it: we live in uncertain times. Many people are spending less and saving more, not just to get ahead, but to protect themselves. The term "revenge saving" emerged after the pandemic, as people began stockpiling emergency funds to regain control.

The old advice used to be: save 3-6 months of expenses. But today? More folks are aiming for 6-12 months. Some are even going for two full years of costs, primarily if they work freelance or have a family to support.

But before jumping to a giant number, take a breath. You don't have to hit a big goal all at once. Start where you are. Build from there.

So, How Much Should I Have in Savings?

Let's break it into three stages:

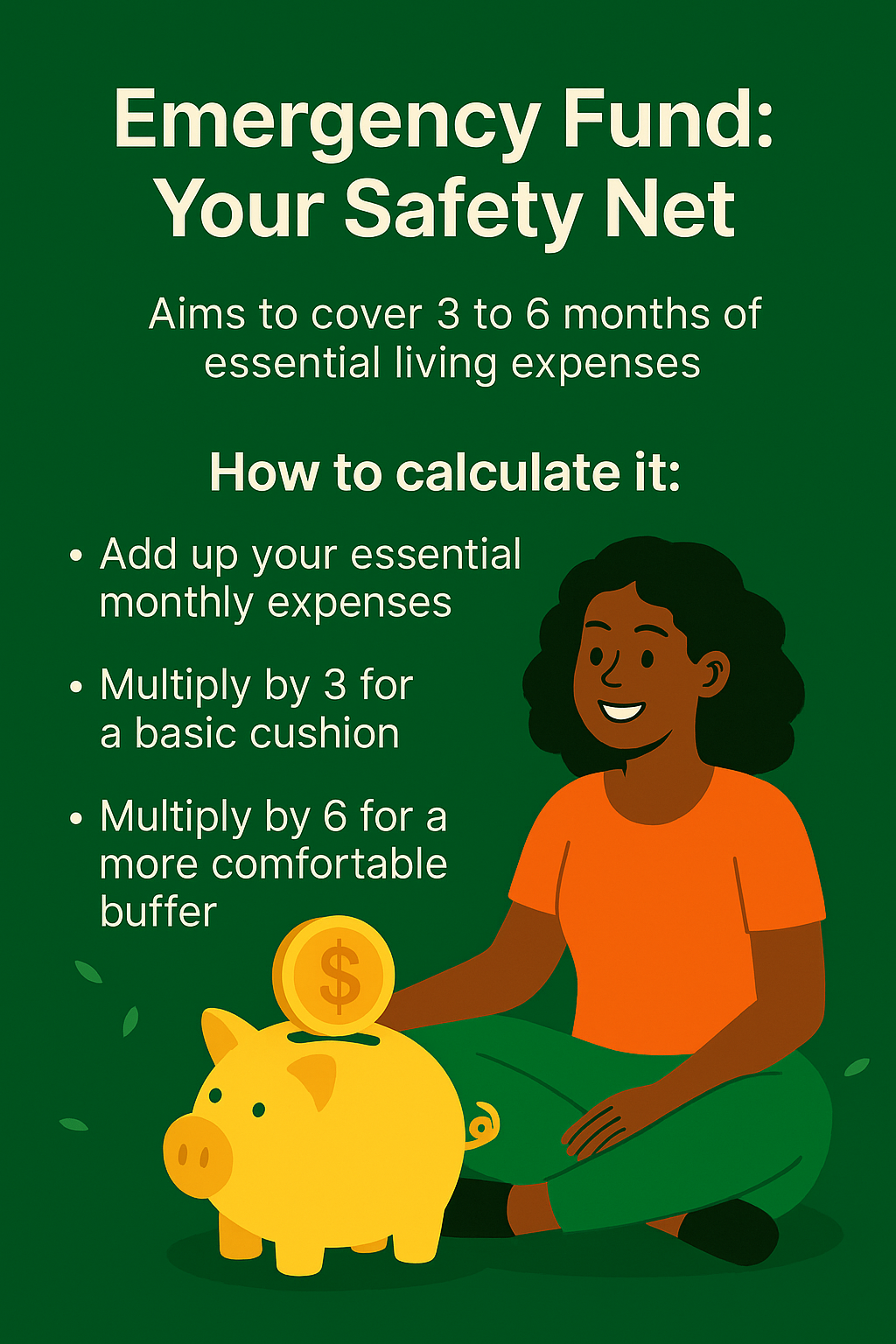

Emergency Fund: Your Safety Net

This is your "just in case" fund. Experts recommend saving 3 to 6 months of your essential living expenses. That includes rent, groceries, insurance, minimum debt payments- anything you'd still have to cover if you lost your income.

How to calculate it:

- Add up your essential monthly expenses.

- Multiply by 3 for a basic cushion.

- Multiply by 6 for a more comfortable buffer.

If your expenses are $2,000/month, your target emergency fund would be $6,000-$12,000.

And if that number feels out of reach? Set a micro-goal: your first $500. Then your first $1,000. You'll get there faster than you think.

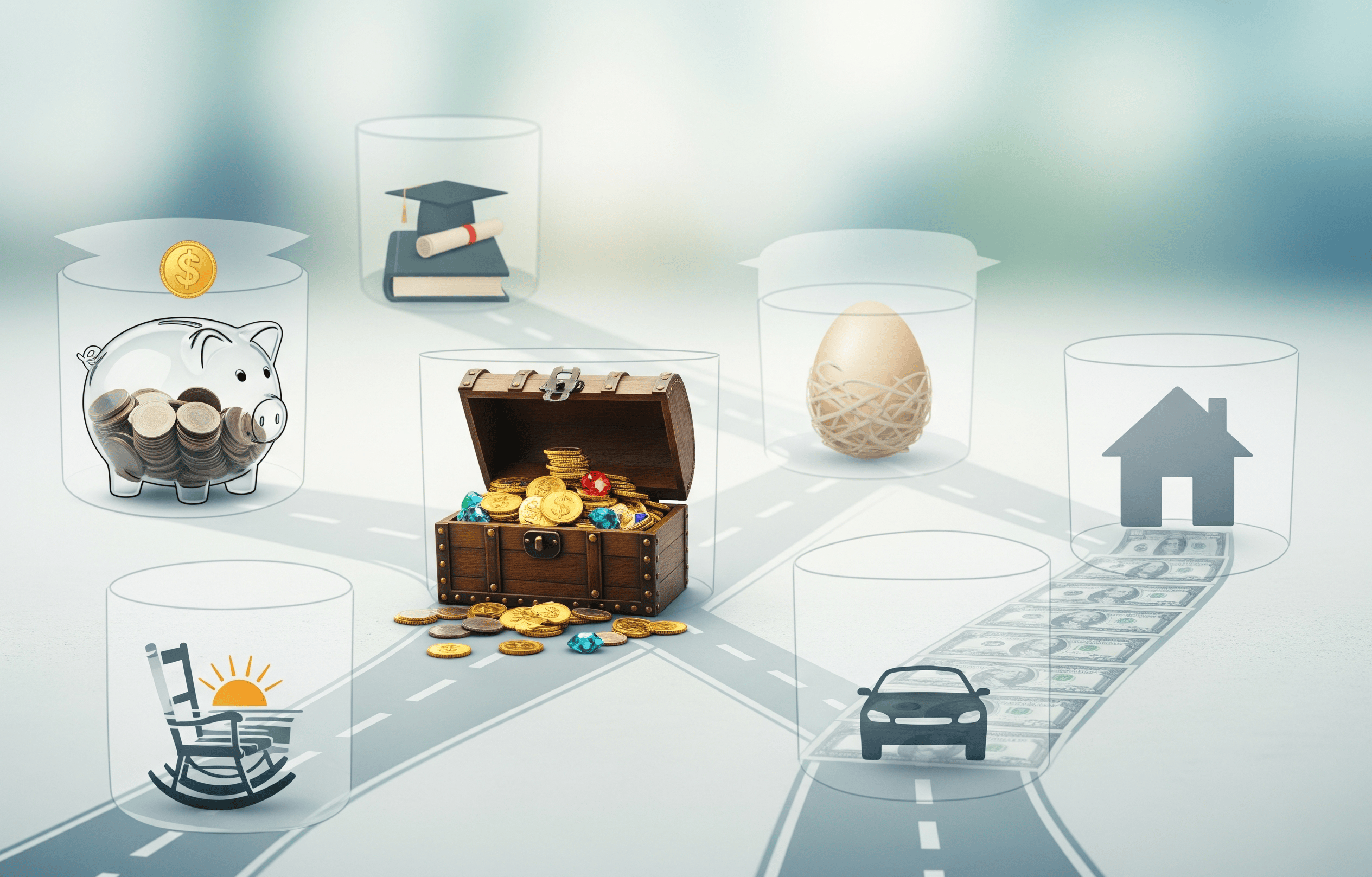

Short-Term Savings: For Life's Known Unknowns

Saving for holiday travel? Moving apartments? Prepping for a wedding or a new laptop? Short-term savings keep you from reaching for a credit card when life happens.

This money should be easy to access, like in a high-yield savings account, but separate from your everyday checking.

Long-Term Savings: Build the Future You Want

Longer-term goals include a house down payment, a business fund, or retirement. These savings may sit in other vehicles, like IRAs, 401(k)s, or investment accounts.

And yes, you can save for these while still building your emergency fund. Think of it like a portfolio of goals. Every dollar has a job.

How Much Should I Save By Age?

If you're wondering whether you're "behind," don't stress. Everyone's path looks different. But these benchmarks can give you a sense of direction:

- By age 30: Emergency fund + 1x your salary saved for retirement

- By 35: 3x your salary

- By 50: 6-8x your salary

- By retirement: 10-12x your salary or 20- 25x your annual expenses

But realistically? Most Americans fall short. Gen Z has an average of $2,410 saved. Millennials hover closer to $23,000. That gap isn't a failure-it's an opportunity to get clear on your next step.

Monthly Savings That Work in Real Life

If saving a significant amount feels out of reach, the best place to start is with a smaller, consistent habit. Even $25 a month can start building your momentum. What matters most is making it automatic. Use direct deposit, recurring transfers, or round-up apps to keep your savings growing quietly in the background. Many financial experts suggest saving 10-20% of your income if possible, but if that's not realistic, start with what you can.

The 50/30/20 rule is a solid framework to try: 50% of your income goes to needs, 30% to wants, and 20% to savings and debt repayment. Fidelity also suggests a 50/15/5 model, allocating 15% toward retirement and 5% toward short-term savings. What's more important than the ratio is the consistency. You're not behind-you're building.

Once You Hit a Goal, Keep Growing

Reaching your emergency fund goal is a huge win. But your money doesn't have to sit still after that. You can keep saving, just with more intention. Start building "sinking funds" for predictable expenses like car maintenance, annual subscriptions, or vacations. That way, these moments don't catch you off guard.

If you've paid off high-interest debt, this may also be the right time to start investing. Even small amounts in a Roth IRA or employer-sponsored plan can grow over time. And if you prefer keeping your savings liquid, consider placing your cash in a high-yield account or CD to earn better interest. Revisit your goals every few months and adjust your plan as life changes-new job, marriage, kids, or relocation. Financial stability isn't static-it evolves with you.

What If I'm Trying To Build Credit Too?

If your savings are growing, but your credit score needs work, you don't have to choose one over the other.

That's where Cheers Credit Builder can help.

With Cheers, you build credit while you save. No membership fees. No setup fees. Just a simple plan that reports your monthly payments to all three major credit bureaus and gives your savings back at the end of the loan.

It's like putting your money to work twice: once for your credit, and again for your future goals.

Get started in minutes—no credit check required.

Final Thought: Build At Your Own Pace

There's no magic number. There's just your number. What makes you feel safe, stable, and empowered? Whether you're starting with $50 or five grand, asking how much you should have in savings is the first step toward something better. And every dollar you save is a step in the right direction.

You've got this.