How much of your paycheck should go to savings? Personal finance advice often tosses around numbers like 10%, 20%, or more, but the truth is, there isn't one fixed rule that works for everyone. This article breaks down the most common savings strategies, including the 50/30/20 and 50/15/5 rules, while also exploring how to build emergency savings, automate your habits, and tailor your approach to inconsistent income. We'll also show how tools like Cheers Credit Builder can help you save money and improve your credit at the same time. Whether you're just getting started or trying to build on progress, this guide will help you find a plan that fits your life.

The Stress: Knowing You Should Save, But Not Knowing How Much

Saving money can be found everywhere, but what no one explains is how you're supposed to do it when your paycheck already feels stretched. You might hear numbers like 10%, 20%, or even 50%. Which one's right? But what if your income is inconsistent or you're paying down rent?

It may be daunting, especially if you're living paycheck to paycheck. However, any small steps now can lead to heightened security down the road. The key is clarity.

The Aspiration: Feeling Confident About Your Financial Future

What if you knew how much to save, without wondering if it's too much or not enough-an automatic savings system. No second-guessing or guilt. Just quiet momentum, building in the background while you live your life.

That's the goal. Not perfection. Not deprivation. Just steady progress.

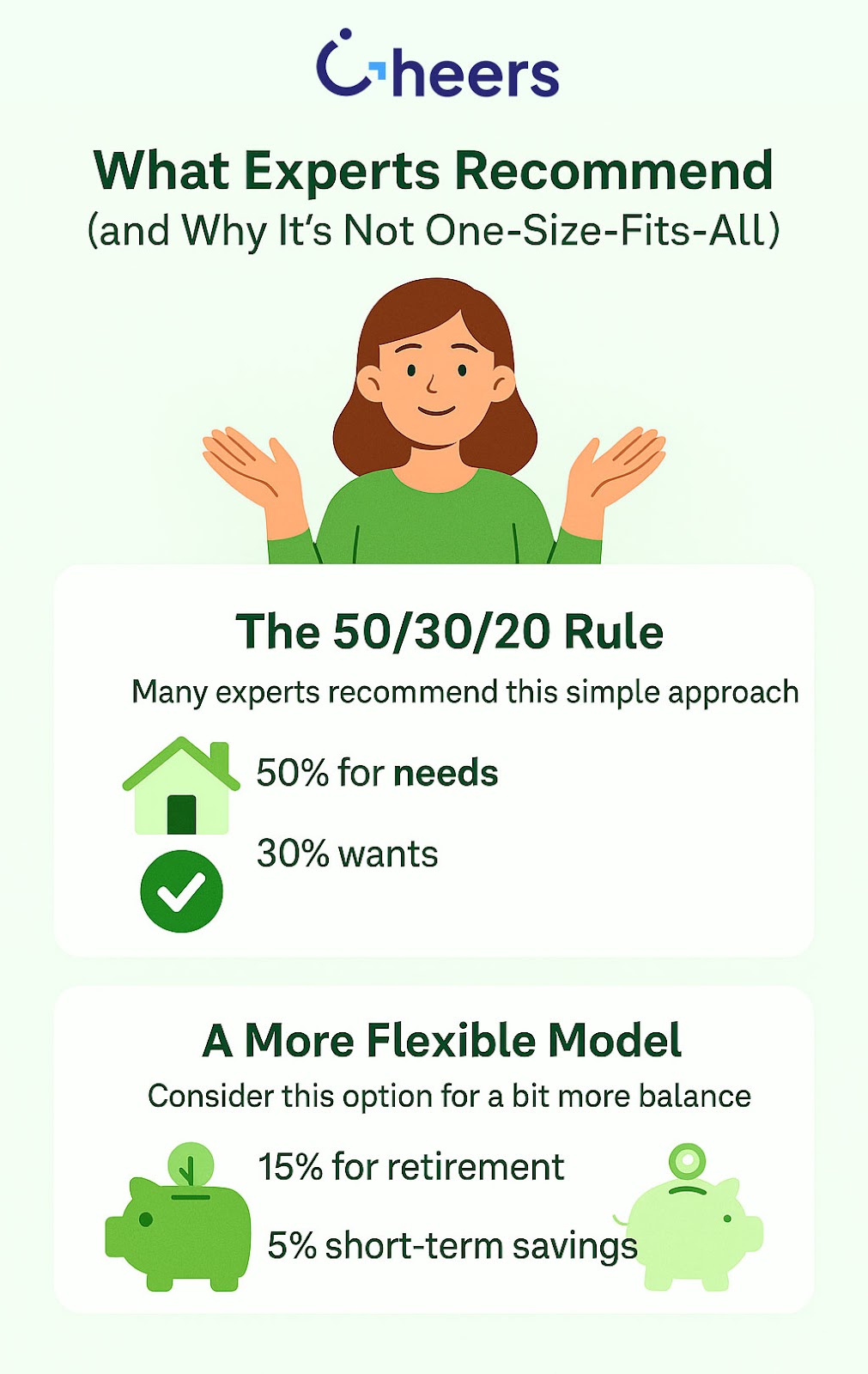

What the Experts Recommend (and Why It's Not One-Size-Fits-All)

The 50/30/20 Rule

It's recommended to try the 50/30/20 framework as a starting point. That means:

- 50% of your take-home pay goes toward needs (like rent, groceries, and transportation)

- 30% goes toward wants (things like dining out, travel, or entertainment)

- 20% goes toward savings and debt repayment

That 20% is your foundation. If you can consistently put aside 20% of your income, you're on track to build a healthy emergency fund, reduce debt, and start investing for the future. However, for many people—especially those with lower or unpredictable incomes—20 % feels out of reach. That's okay. Starting small still counts.

A More Flexible Model: The 50/15/5 Rule

Another recommendation: 15% for retirement, 5% for short-term savings. This version separates long-term and emergency savings, so you're not pulling from one bucket when something unexpected happens.

The point isn't which rule is better. It's about selecting a target that aligns with your life right now and building from there.

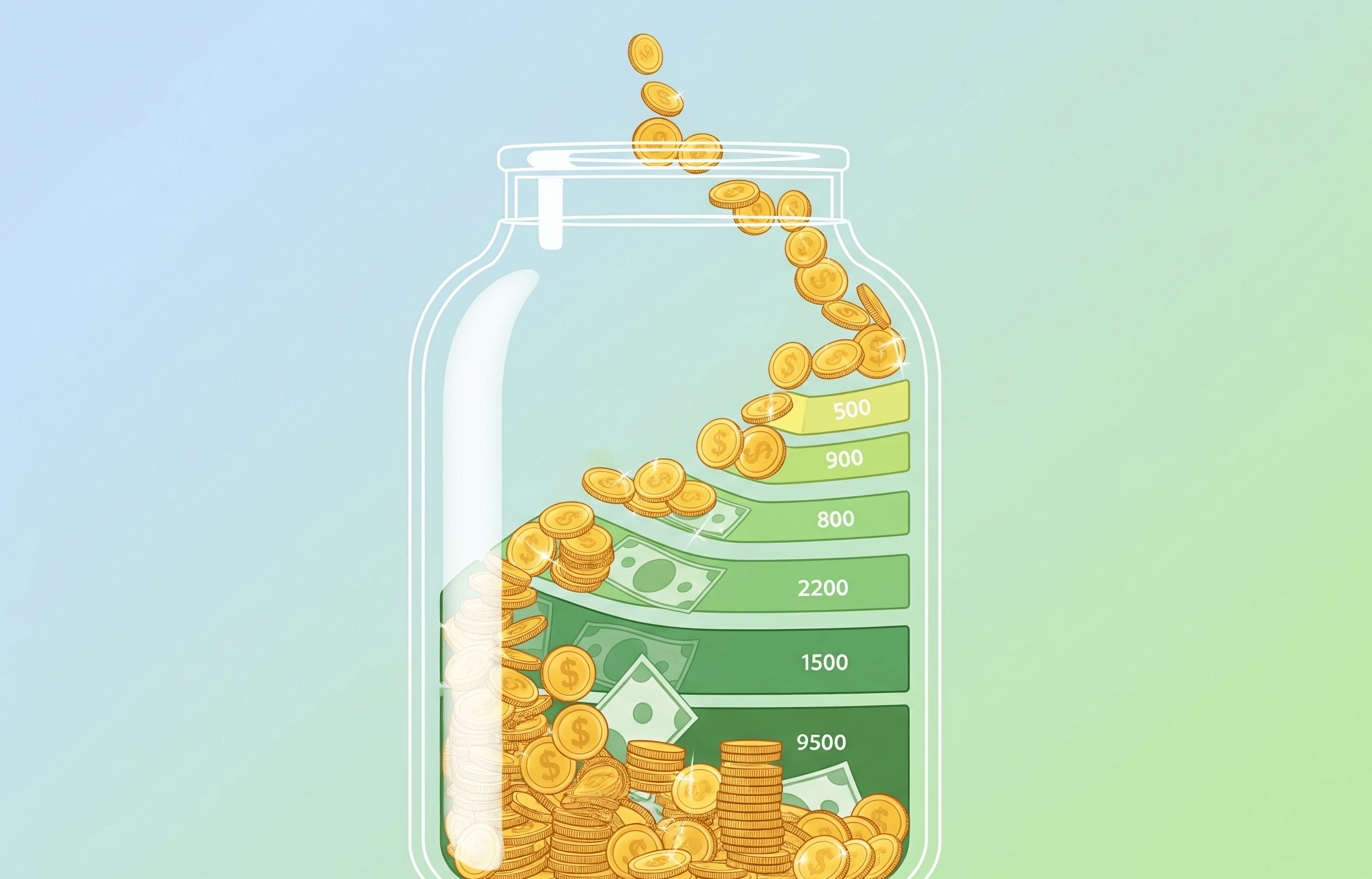

Your First Target: Emergency Savings

While considering investing or saving for a home, your priority should be managing your cash. Specifically, money that you can access immediately in case of an emergency.

It's recommended to start with $500 to $1,000 if you're beginning. Once you've established that buffer, aim to save 3-6 months' worth in an essential expenses savings account.

Even saving $25 or $50 per paycheck adds up. The sooner you start, the more protected you'll feel. And with tools like Cheers Credit Builder, you can build savings and credit at the same time.

Automate It: Paying Yourself First

Experts across the board, including Investopedia, agree: the easiest way to save consistently is to pay yourself first. That means you set aside savings right after your paycheck hits, before spending on anything else.

If you wait to see what's left over at the end of the month, there's a good chance it'll be nothing. But if you move that money into savings automatically, you won't miss it, and over time, it'll grow.

Start with a percentage you can handle. Even 5-10% is better than nothing. Then increase it every few months until you hit your target.

The Reality: Income Isn't Always Steady

Gig workers, freelancers, and individuals with variable incomes often struggle to follow rigid percentages. It's recommended to plan around your lowest expected income. Build your monthly budget based on that number. If you earn more, funnel the extra money into savings or debt repayment.

Some people find it helpful to create two bank accounts: one for "bare bones" expenses and another for savings. That separation alone can help you spend more intentionally.

Your Game Plan

Start by figuring out exactly what your take-home pay is-what you bring home after taxes. That number becomes your foundation. Then, choose a savings percentage that works for your current situation. If 20% feels like too much, that's okay. Even starting at 5% or 10% can get you moving in the right direction. The goal isn't to hit a perfect number on day one-it's to start building the habit.

Next, automate it. Use your bank or an app to transfer that savings amount into a separate account every time you get paid. That removes the decision-making and temptation from the equation. If you don't see the money sitting in your checking account, you're less likely to spend it.

Once your emergency fund hits $1,000, aim for three to six months of living expenses. That savings cushion gives you breathing room during layoffs, car repairs, or medical bills. And don't forget to revisit your savings rate every few months. If your income increases or your expenses drop, consider boosting your contributions. Little changes over time can add up to a significant difference.

Finally, build a system that works for you, not just a generic blueprint. If you prefer visual motivation, track your savings goals. If you work on commission, base your savings on a percentage of each check instead of a fixed dollar amount. Customizing the process makes it easier to stick with over time.

How Cheers Credit Builder Helps You Save Smarter

If saving and building credit feel like two separate challenges, Cheers Credit Builder brings them together.

With flexible monthly plans starting as low as $24/month, Cheers helps you build credit by reporting payments to all three major credit bureaus. But here's the twist: every payment you make goes into an FDIC-insured savings account. At the end of your loan term, you will receive the money back, minus interest.

That means you're not just building your credit score-you're saving money at the same time. And because there's no credit check, no admin fees, and no membership charges, it's simple to start even if you're brand new to personal finance.

It's automated, consistent, and reports faster than most credit builder programs. You can sign up in minutes, choose your plan, and start building credit while saving real money.

You Don't Need to Be Perfect-You Need to Start

No magic number works for everyone. Some months, saving 10% of your paycheck is impossible. Others, you'll be able to do more. What matters is starting with something, automating it, and increasing it over time.

The question isn't just "how much of my paycheck should go to savings?" It's: "How can I make savings a habit that fits my life?" Because once you answer that, you stop wondering and start building.