What Is the Average Retirement Savings at Retirement?

The average retirement savings at retirement in the U.S. often falls short of what’s needed to stop working comfortably. While averages vary across reports, Vanguard found that people aged 65 and older have an average 401(k) balance of about $232,710. However, the median balance—what most people actually have—is only around $70,620. That’s a big gap.

Data from the Federal Reserve also shows that many nearing retirement have saved less than they’ll need. For people aged 55–64, the median savings is about $185,000.

The phrase “average retirement savings at retirement” sounds simple, but the reality is far more uneven. Some Americans retire with over $1 million. Others have nothing.

Why the Numbers Are So Different

Averages don’t always reflect reality. High-income earners with large balances can skew the average upward. That’s why the median savings is often a better way to understand what typical people have.

Why are so many Americans behind?

- Many don’t have access to a retirement plan at work

- Others start saving late due to student loans or low wages

- The rising cost of housing and healthcare eats into what people can set aside

- Some withdraw early due to emergencies or job loss

According to the U.S. Census Bureau, around 49% of adults between 55–66 have no personal retirement savings at all. That’s almost half the population approaching retirement with little to fall back on.

Breakdown of Retirement Savings by Age

Let’s look at what average retirement savings at retirement—or leading up to it—look like by age. These numbers come from recent studies by Fidelity and the Census Bureau.

- Under 35: Median retirement savings of about $11,000

- Ages 35–44: Around $28,000

- Ages 45–54: Roughly $48,000

- Ages 55–64: About $185,000

- 65 and older: Median balance of $70,620

Fidelity also recommends that you have about 10 times your salary saved by age 67. But many fall short of that benchmark.

How Much Should You Save for Retirement?

Experts suggest aiming to replace about 70% to 80% of your annual income each year in retirement. For example, if you earn $60,000 a year, you’d need $42,000–$48,000 per year after you stop working.

A common rule of thumb is the 4% rule. If you withdraw 4% of your savings annually, your money may last around 30 years. That means to generate $40,000 a year, you'd need at least $1 million saved.

But reaching that number is hard. According to the Transamerica Center for Retirement Studies, only 27% of workers in their 60s have saved $250,000 or more. Most people are behind.

This is why the average retirement savings at retirement matters so much. It’s a reality check—and a reason to start planning now.

Why Credit Still Matters in Retirement

Even as you age, credit health continues to affect your financial options. Your credit score can influence:

- Your ability to refinance your mortgage

- Approval for personal loans or credit lines

- Insurance premiums and deposit requirements

For people in their 40s and 50s, working to raise their credit score now can unlock lower interest rates, freeing up more room to save for retirement. It’s also helpful in retirement if you face unexpected medical bills or emergencies.

Improving your credit doesn’t have to mean taking on debt. It’s more about showing consistent, on-time payments and maintaining a healthy credit mix.

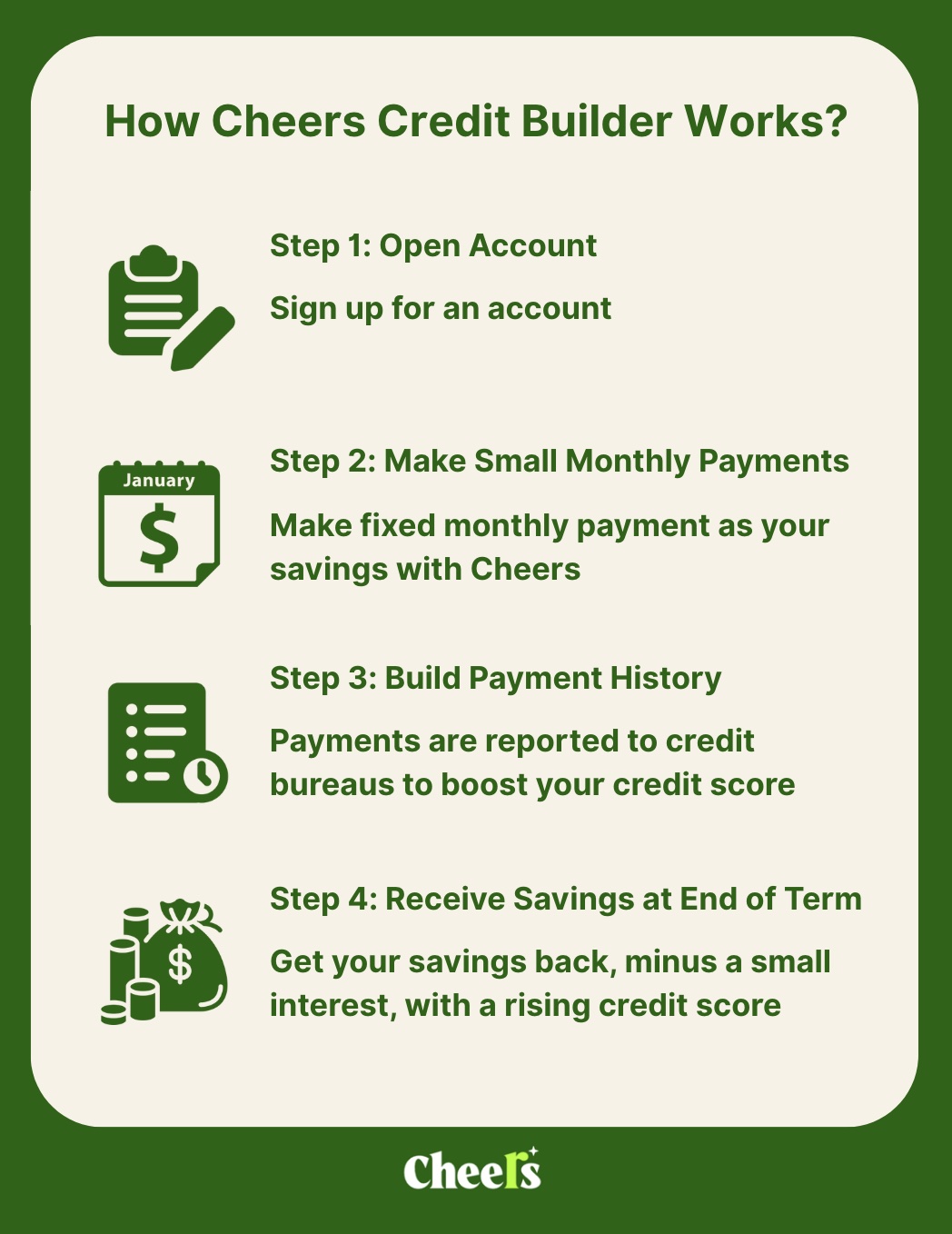

How Cheers Can Support Your Financial Growth

If you’re building credit while trying to grow your savings, a product like Cheers Credit Builder makes it easy. Cheers helps you build credit automatically, without the need for a credit card. Your monthly payments are reported to all three major credit bureaus. These payments are stored in an FDIC-insured account and returned to you (minus interest) after the term ends.

Cheers is simple to use—no membership fees or hidden charges. You pick a repayment plan that works for your budget, from 12 to 24 months. It’s designed to support people who are new to credit, rebuilding, or just trying to improve their financial standing ahead of retirement.

Final Thoughts

The average retirement savings at retirement is a reminder of how uneven the landscape is. Whether you’re in your 20s or 50s, it’s not too late to make smart changes. Build your savings. Improve your credit. Keep learning and adjusting.

And if you want easy, automatic tools to help you grow your financial future, sign up for the Cheers newsletter. We share credit tips, saving strategies, and insights that make your money work smarter.

References:

- Vanguard – How America Saves (2024)

https://corporate.vanguard.com/content/dam/corp/research/pdf/how_america_saves_report_2024.pdf - Federal Reserve – Report on the Economic Well-Being of U.S. Households (2023)

https://www.federalreserve.gov/publications/2024-economic-well-being-of-us-households-in-2023-executive-summary.htm - Fidelity – How Much Money Do I Need to Retire?

https://www.fidelity.com/viewpoints/retirement/how-much-money-do-i-need-to-retire - Transamerica Center for Retirement Studies – 23rd Annual Retirement Survey

https://www.transamericacenter.org/