Author: Vince Adriatico (Ex-banker with 750+ Credit Score)

Date: 5/13/2025

Table of Contents:

- Where Housing Prices Stand in 2025

- The Highest and Lowest Average Housing Costs by State

- Income vs. Cost: Where the Math Works-and Where It Doesn't

- How Regional Trends Are Shaping Buyer Behavior

- Renters Are Feeling the Squeeze, Too

- What First-Time Buyers Should Expect

- What Comes Next for the Housing Market

Whether you're moving across the country or just trying to figure out how far your paycheck can stretch, knowing the average housing cost by state is a smart place to start. The cost of housing isn't just a real estate stat- it's one of the most significant forces shaping where and how people live. And right now, there's a wide gap between the most and least affordable states.

In 2025, average home prices in the U.S. hover around $503,800, while the median sits closer to $416,900. But zoom in a little, and the picture shifts. A house under $200,000 in West Virginia might cost over $800,000 in Hawaii. Income levels, housing demand, interest rates, and job markets play into the price tag but don't play out equally everywhere. This article explores what those numbers look like, how affordability ties into income, and what today's buyers and renters are up against as they try to find a foothold in the housing market.

Where Housing Prices Stand in 2025

Across the country, average home prices reflect a mix of cooling markets and stubbornly high costs. After rapid appreciation, some cities have seen modest dips while others continue climbing. However, despite those shifts, the average housing cost by state remains out of sync with income in many areas.

At the national level:

- The average U.S. home price is about $503,800.

- The median home price is $416,900.

- Due to higher interest rates, many buyers are putting down more than 20% to reduce monthly costs.

The pressure of affordability isn't spread evenly. While some regions are seeing demand, particularly in tech-heavy metros where remote work has taken place, other areas still see inventory shortages push prices higher.

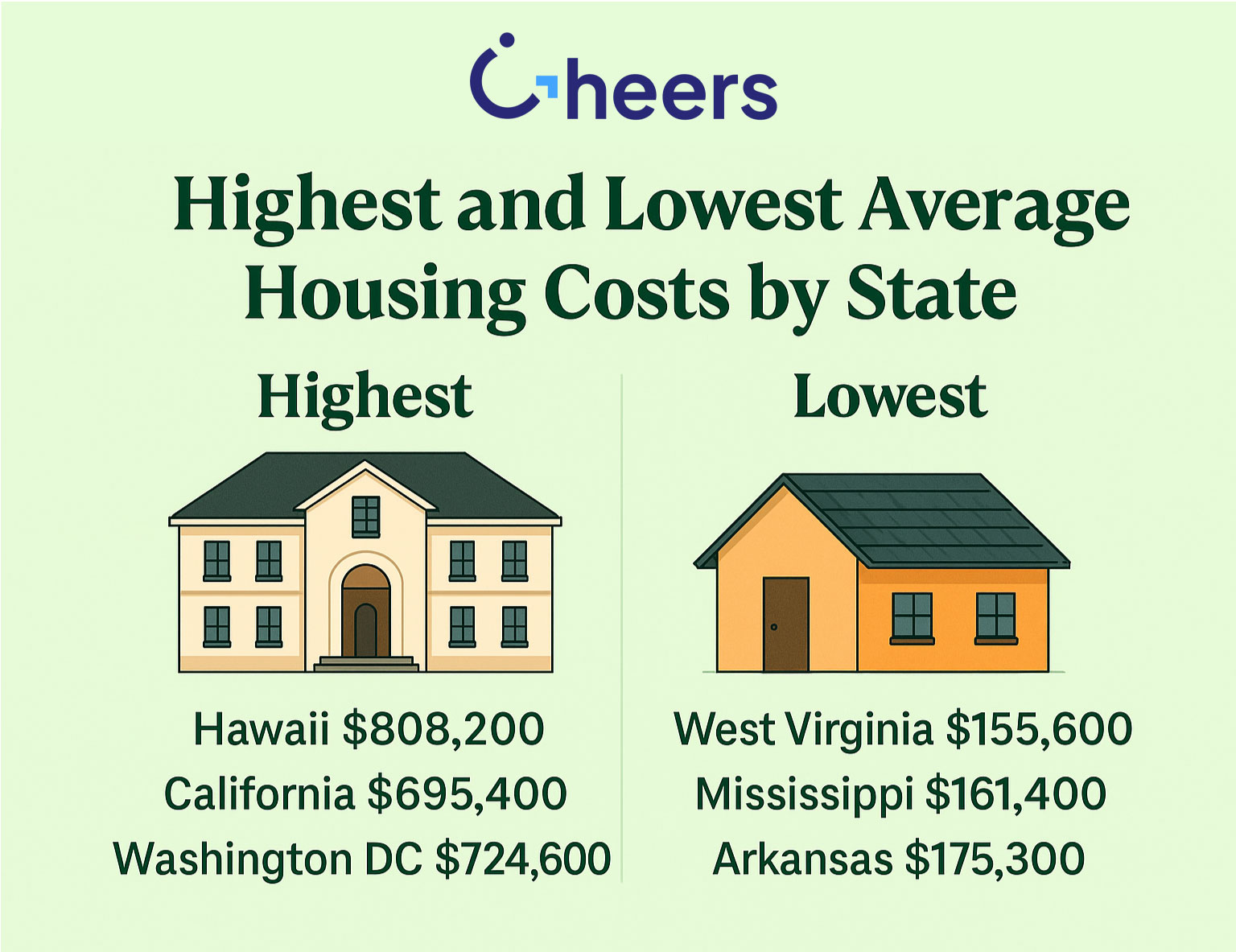

The Highest and Lowest Average Housing Costs by State

Geography plays the most significant role in what buyers and renters can expect to pay. The average housing cost by state varies by hundreds of thousands of dollars, depending on where you live.

In the most expensive states:

- Hawaii averages around $808,200 for a single-family home.

- California comes in at about $695,400.

- Washington, D.C., sits close to $724,600.

These states reflect high demand, limited inventory, and lifestyle appeal. However, they also reflect a larger gap between wages and housing access.

At the other end of the spectrum:

- West Virginia has an average home price of about $155,600.

- Mississippi sits around $161,400.

- Arkansas averages $175,300.

In these areas, wages are also lower, as is the entry barrier. Starting in one of these more affordable markets can make a big difference for people building credit or looking to move into homeownership.

Income vs. Cost: Where the Math Works-and Where It Doesn't

Looking at prices alone doesn't tell the full story. You also have to factor in what people earn. In California, where the median home price is over $794,000, the average household income is $84,907. That puts the price-to-income ratio at 9.35. That means the typical buyer would need nearly 10 years of full income to match the price of a home.

Compare that to Ohio, where the median home price is $228,000 and the average income is $62,262. That ratio is closer to 3.6, which is far more manageable-even with interest rates above 6%.

Planning for homeownership is not just about getting pre-approved or saving for a down payment. It's about evaluating the whole picture: monthly costs, interest rates, property taxes, and how much of your income goes to housing. For many Americans, those numbers are starting to get tight.

How Regional Trends Are Shaping Buyer Behavior

State-by-state cost data shows that buyers are shifting where they look for homes. Some are leaving high-cost cities for more space and less stress in smaller metro areas. Others are relocating for remote jobs, targeting states where their income will increase.

For example, markets like Austin and Dallas have started to cool in Texas. While still not "cheap," median prices have dropped slightly, and mortgage payments have followed. The state's population growth and new construction have helped temper the demand.

In California, the opposite remains true. Despite some softening in certain metros, the state remains one of the least affordable places to live. In many counties, buyers spend 40% or more of their income on housing above the 30% guideline often recommended for affordability.

The Midwest and South continue to draw buyers looking for stability and lower costs. States like Iowa, Missouri, and Oklahoma offer a more balanced income ratio to housing prices, especially for first-time buyers trying to enter the market.

Renters Are Feeling the Squeeze, Too

You don't need to buy a home to feel the impact of rising costs. Renters are facing a different version of the same problem. Since 2020, average rents have increased by 29% across the country. In contrast, household income has risen by only 22.5% in the same time.

In cities like San Antonio, average rent now requires an annual income of over $58,000 to remain affordable by federal standards. That leaves many renters choosing between moving farther from city centers, downsizing, or spending a larger share of their income on housing.

Credit building becomes even more critical in this environment. As rental costs increase, renters who want to transition into homeownership need to strengthen their financial position. Positive payment history, lower credit utilization, and a solid mix of credit types can help open doors that would otherwise stay closed.

What First-Time Buyers Should Expect

The dream of owning a home is still alive but comes with more homework than ever. Across all states, the average first-time buyer down payment is now about $12,274. That doesn't include closing costs, which average just under $2,000.

In high-cost states, down payments can easily hit $40,000 to $50,000. Without outside support, many buyers rely on savings accounts, side hustles, and alternative tools, such as credit builder loans, to show lenders they're ready for the responsibility.

Programs like Cheers Credit Builder make preparing for the financial steps required in today's market easier. Because Cheers reports to all three credit bureaus and starts building payment history on Day 1, users have a faster runway to improve their scores, often before they even reach the point of mortgage pre-approval.

What Comes Next for the Housing Market

Predictions for 2025 suggest that home prices will continue to rise- just not as quickly. The National Association of Realtors projects a 2% increase in median prices over the next year. That might sound small, but that could still add tens of thousands to a home's sticker price in high-cost areas.

Meanwhile, affordability remains the biggest challenge for most Americans. As wages struggle to keep pace with housing costs, more people are rethinking what homeownership should look like. They're looking at smaller homes, longer commutes, multi-generational living, or out-of-state moves as practical ways to make it work.

Being financially prepared has never mattered more. Understanding the average housing cost by state, knowing your numbers, and building your credit are your strongest tools if you want to make a smart move, now or later.