Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 5/25/2025

Table of Contents

- What Is Annual Income?

- Gross vs. Net Annual Income

- Why Annual Income Matters

- How to Calculate Annual Income

- What to Include and What to Skip

- Annual Income and Credit Applications

- Start Building Credit With Your Income

What Is Annual Income?

Annual income is the total amount of money you earn in a year. It includes everything from wages and salaries to tips, freelance payments, and bonuses. Whether you’re a salaried employee or juggling multiple part-time gigs, your annual income is a key number in your financial life.

You’re often asked to provide your annual income on applications—like credit cards, car loans, or rental forms. So, it helps to know exactly what counts, how to calculate it, and why it matters.

According to the Consumer Financial Protection Bureau (CFPB), annual income can be reported in different ways depending on the purpose. Still, it should reflect your ability to repay debt or meet financial obligations.

Gross vs. Net Annual Income

The first thing to understand is the difference between gross annual income and net annual income.

Gross income is the total you earn before any deductions. This includes taxes, Social Security, health insurance, and retirement contributions. If Adrian earns $65,000 from her full-time job, that’s her gross income.

Net income is what she takes home after those deductions. If she pays $13,000 in taxes and benefits, her net annual income is $52,000. Many financial decisions, such as budgeting, are based on net income, whereas lenders often consider gross income.

Why Annual Income Matters

Your annual income affects what you qualify for. Lenders use it to estimate your ability to repay loans. Landlords consider it when evaluating rental applications. Government agencies may use it to determine if you’re eligible for programs like student aid or Medicaid.

Let’s say Adrian applies for a personal loan. Her annual income is a major part of the application. Combined with her credit score, it helps lenders decide how much she can borrow and at what interest rate. According to Fannie Mae, your income plays a role in your debt-to-income (DTI) ratio, which is a key metric for approving mortgages.

How to Calculate Annual Income

To find your annual income, start with your regular earnings and multiply it to cover the whole year. If you're paid hourly, multiply your wage by the number of hours you work per week, then multiply that by 52.

Example:

Adrian works 35 hours per week at $20/hour.

$20 × 35 = $700/week

$700 × 52 = $36,400 gross annual income

If she earns tips or side income from freelance work, she should include that as well. Bonuses, commissions, and part-time jobs also count.

To get a better estimate of what your take-home pay looks like, use the IRS tax withholding estimator.

What to Include and What to Skip

When asked, “What is annual income?”—the answer depends on what’s included.

Include:

- Wages or salary

- Overtime and bonuses

- Freelance or contract earnings

- Rental income or business income

- Unemployment benefits (if taxable)

- Tips or commissions

Don’t include:

- Scholarships or grants (unless taxable)

- Loans or gifts

- Child support (not considered income by lenders)

- Non-taxable reimbursements

Be sure to check how the income is defined for whatever you’re applying for. Income considered for tax purposes may differ from income considered for loan approval.

Annual Income and Credit Applications

When applying for credit, your income can be as important as your credit score. Lenders use it to assess whether you can afford monthly payments.

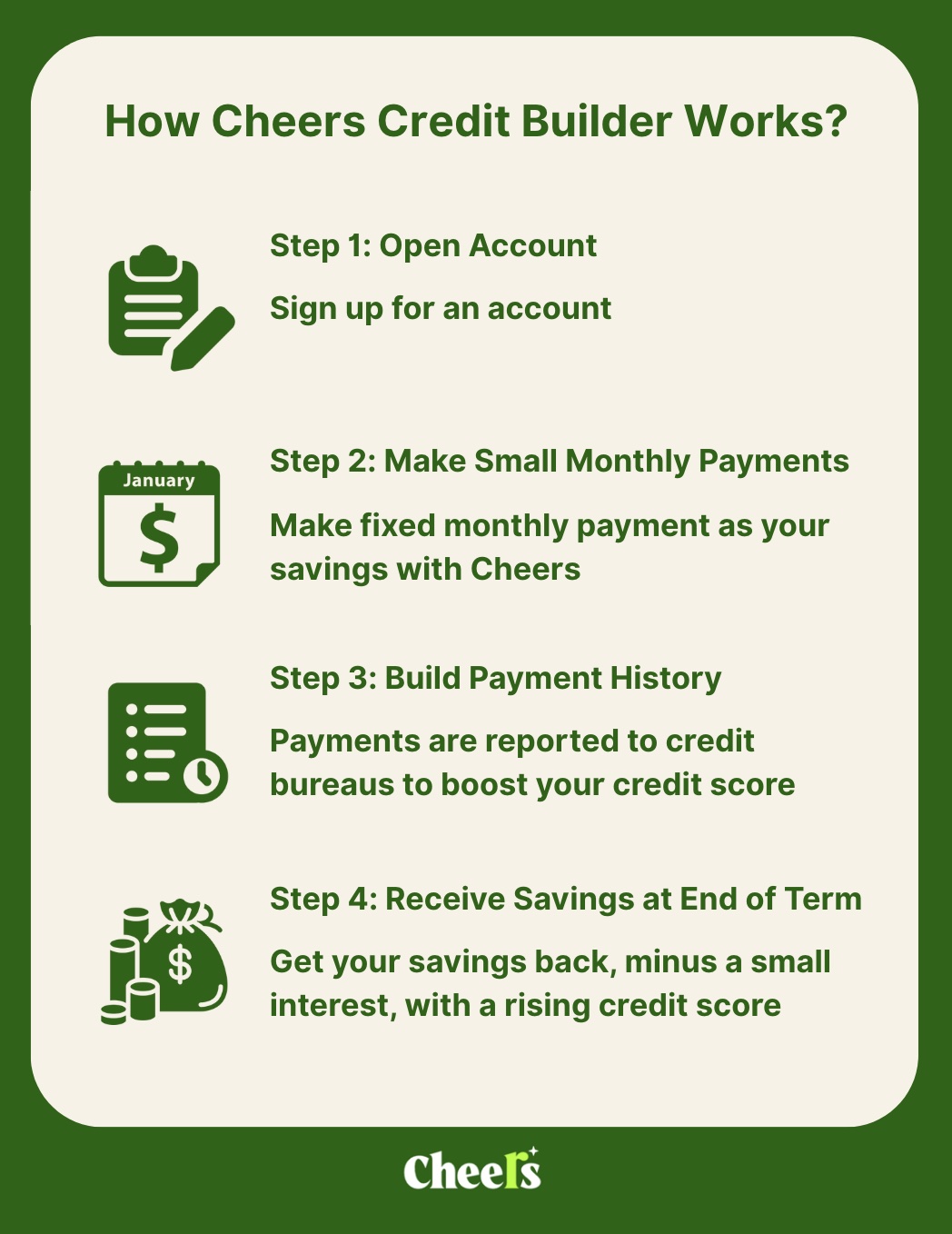

If Adrian is applying for a credit builder loan, she might be asked to report her annual income. Even if her income isn’t high, showing consistent earnings helps build trust with lenders. Some financial tools—like the Cheers Credit Builder—don’t require a credit check and are designed for people who want to build credit using installment loans.

Cheers reports on-time payments to all three major credit bureaus. This can help establish payment history, which makes up a large part of your credit score, according to Experian.

Start Building Credit With Your Income

Understanding what annual income is can help you take more control over your financial decisions. Whether you’re planning your first budget, applying for a student loan, or trying to improve your credit, knowing your income is the first step.

Cheers Credit Builder is a simple way to turn that income into progress. You select a plan, make monthly payments, and build credit without the need for a credit card. There’s no setup fee, no membership fee, and no hard pull on your credit report—just steady progress, reported every month.

Cheers is not a bank. Deposit accounts held by partner bank, Member FDIC.

Reference

- Consumer Financial Protection Bureau - Mortgage Key Terms

- Fannie Mae - Selling Guide

- IRS - Tax Withholding Estimator

- Experian - What Affects Your Credit Scores?