Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 5/24/2025

Table of Contents

- What Is a Guarantor?

- Why Lenders Require Guarantors

- Adrian’s Experience With His First Apartment

- Guarantor vs. Co-signer

- Risks of Being a Guarantor

- Do You Need a Guarantor to Build Credit?

- Final Word

What Is a Guarantor?

If you’ve ever applied for a loan or apartment and been told you need a guarantor, you’re not alone. So, what is a guarantor exactly? A guarantor is an individual who promises to assume responsibility for a loan or agreement if the original borrower fails to fulfill their obligations. Guarantors are often used in rental contracts, personal loans, and some credit-building options.

This person typically doesn’t receive any financial benefits. Instead, they offer assurance to lenders or landlords that the financial obligation will be met. A guarantor normally has good credit and a steady income. Their promise helps make risky applicants more acceptable to lenders. You can find more background about this on Experian’s page on guarantors.

Why Lenders Require Guarantors

Lenders ask, What is a guarantor needed for? Typically, this occurs when the borrower has no credit history, a low income, or a history of missed payments. A guarantor reduces the lender’s risk by stepping in if something goes wrong.

This issue arises frequently for recent graduates, young adults, or individuals new to the U.S. They may not have had sufficient time to establish credit, despite having a stable income. Landlords and financial institutions use guarantors as backups to ensure payments won’t be missed.

The Consumer Financial Protection Bureau offers helpful information on why lenders use guarantors and how these agreements work.

Adrian’s Experience With His First Apartment

To make it more relatable, here’s a story about my friend Adrian. He had just moved to Chicago for grad school and was excited about getting his own place. But when he applied, the landlord said he needed a guarantor. Adrian had just started his credit journey and didn’t meet the income requirement.

His cousin, who had a long credit history and a steady job, stepped in as a guarantor. That made the difference — Adrian got the apartment. His cousin didn’t have to pay anything upfront, but legally agreed to cover the rent if Adrian ever fell behind. That’s the core of what being a guarantor means: you’re stepping in with trust, not cash — unless the borrower defaults.

Guarantor vs. Co-signer

People often ask: What is a guarantor compared to a co-signer? While similar, they’re not the same. A co-signer is on the hook from day one. Their credit gets used right away, and they’re treated as a joint borrower. A guarantor, however, only comes into play if the borrower fails to pay.

For example, in a student loan, a co-signer shares full liability for the balance. But if someone guarantees a rental lease, they’re only responsible if rent goes unpaid. Bankrate explains the difference clearly with the pros and cons of each.

Risks of Being a Guarantor

Being a guarantor can feel like a favor — but it’s a serious financial responsibility. If the borrower defaults, the guarantor has to repay the debt. That could harm their credit score, increase their debt-to-income ratio, or result in legal consequences.

Even if payments are made on time, the agreement may still show up on the guarantor’s credit report. That could impact their future borrowing capacity. It’s wise to carefully review every detail of the agreement before signing. NerdWallet provides a helpful guide on what to consider before agreeing to become one.

Do You Need a Guarantor to Build Credit?

Sometimes people ask: What is a guarantor’s role in building credit? In many cases, guarantors help borrowers qualify for loans that report to credit bureaus. But there are ways to build credit without needing a guarantor.

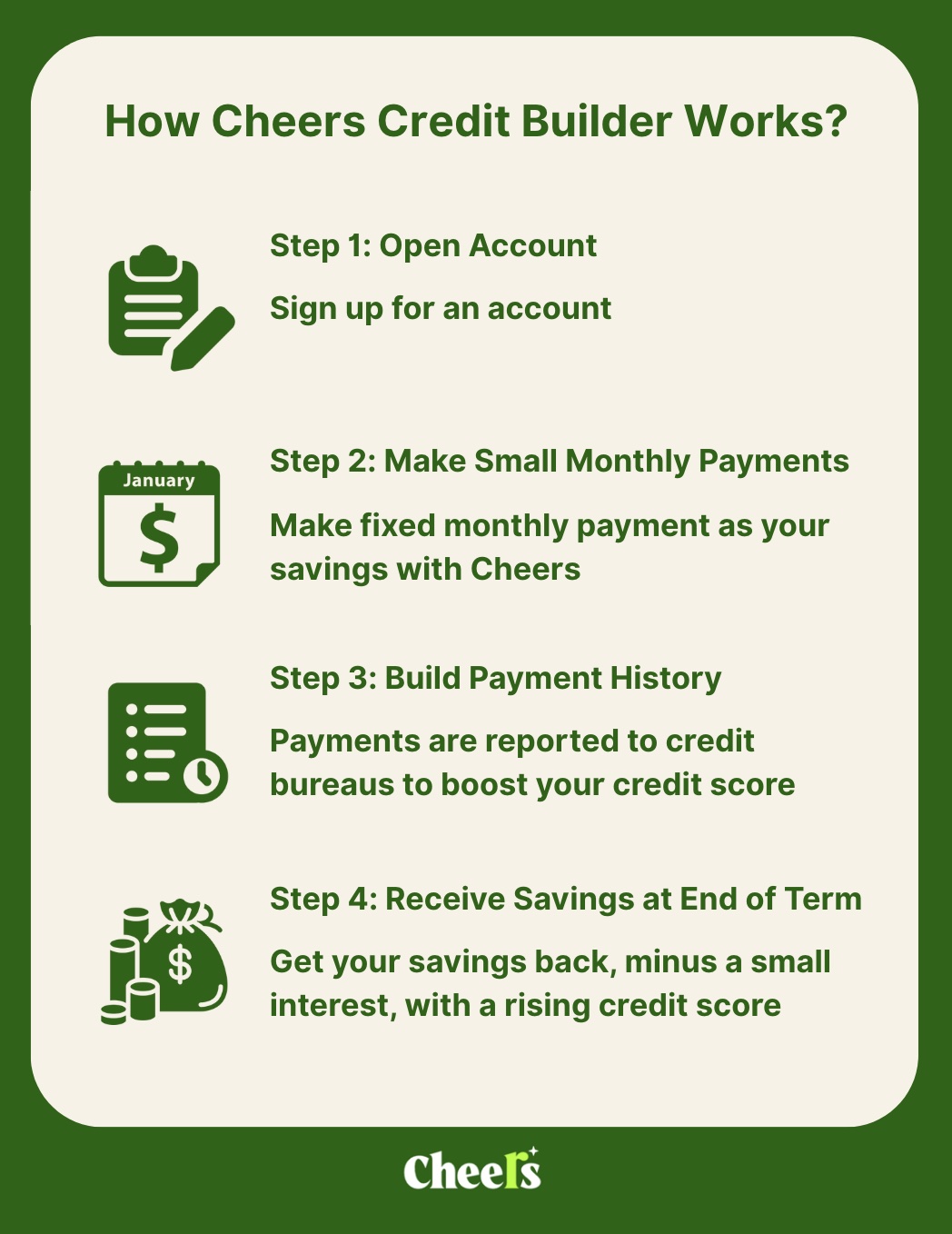

The Cheers Credit Builder, for example, allows you to build credit history by reporting your monthly payments to all three major credit bureaus, without requiring a co-signer or guarantor. You choose a loan amount and repayment term that fits your goals. Your payments are held in an FDIC-insured account, and you get that money back at the end, minus interest.

Unlike other credit-builder loans that take a month to report your first payment, Cheers starts reporting the next business day. That means you can build a payment history, which makes up 35% of your credit score, faster. There’s no setup or membership fee, just a small interest.

To learn more about building credit safely, check the Federal Reserve’s credit guide.

Final Word

What is a guarantor? It’s someone who backs you up financially when you need a helping hand. Whether it’s for a loan, apartment, or credit application, having a guarantor can open doors. But it’s not without risk. If you’re considering asking someone to be your guarantor — or thinking about saying yes — it's essential to understand the responsibilities it entails.

If you want to build credit without asking someone else to step in, Cheers Credit Builder is a smart alternative. It’s built for people starting from scratch or rebuilding after setbacks — no guarantor needed.

Reference:

- Experian - What Is a Guarantor for an Apartment and Do I Need One?

- Consumer Financial Protection Bureau - Comment for 1002.7 - Rules Concerning Extensions of Credit

- Bankrate - Cosigner rights & responsibilities: How cosigning works

- NerdWallet - Who can be a Guarantor for a Loan?

- Federal Reserve Board - Credit Reports and Credit Scores