Understanding what the current balance means is a key step in managing your credit. Your current balance reflects the total amount you owe on your credit card or loan account at a specific point in time. It includes posted transactions, pending charges, payments, and any fees or interest that have been added since your last billing cycle.

Unlike your statement balance, which is fixed at the end of each billing period, your current balance changes often. If you make purchases, pay off part of your bill, or even incur a late fee, those changes are reflected immediately in your current balance.

If you're tracking your credit card usage or trying to pay off debt, knowing your current balance helps you avoid surprises and manage your spending effectively. According to Bankrate, this real-time number gives you a more accurate picture of your finances.

Current Balance vs. Statement Balance

The statement balance is what you owe at the end of your last billing cycle. It's the number you see on your monthly credit card bill. The current balance, however, is your running total of all unpaid charges—including any charges that occurred after the statement closed.

Let's say your credit card statement ended on June 1 with a balance of $300. On June 2, you bought something for $50 and made a payment of $100. Your current balance is now $250. That's the amount you'd need to pay to wipe your account clean completely.

While credit bureaus like Experian, Equifax, and TransUnion typically receive your statement balance once per month, your current balance still plays a role in managing your credit wisely. It reflects how much of your available credit you're using in real-time.

Why Your Current Balance Changes Often

Every time you make a purchase or payment, your current balance changes. That’s because it reflects what’s happening now, not just what happened during your last billing cycle. The current balance will also rise if you’re charged interest or fees.

Here’s what might be included in your current balance:

- New purchases or cash advances

- Pending transactions waiting to post

- Interest charges from carried balances

- Payments or credits that have been applied

- Fees like late charges or annual fees

While some banking apps may break these out separately, your total current balance usually includes all these elements. That’s why it can shift daily—even hourly.

Credit Score Impact from Your Current Balance

Your credit utilization ratio—how much of your credit limit you're using—has a significant effect on your credit score. Most lenders recommend keeping that usage below 30% of your credit limit. A high current balance, even if temporary, could push you above that threshold.

Credit scoring models, such as FICO and VantageScore, consider utilization one of the most influential factors. So even if your current balance isn't reported to credit bureaus, it reflects how you manage your credit in real-time—and lenders do pay attention.

If your current balance gets too high, it can raise red flags when you apply for a new loan or line of credit. That's why regularly monitoring it's helpful, especially if you're rebuilding or just beginning your credit journey.

How to Handle Your Current Balance Smartly

Here are simple ways to keep your current balance in check:

- Check your current balance at least once a week through your credit card’s app or website

- Try to pay off your current balance in full if you can, not just the statement balance

- Set spending limits to avoid creeping too close to your card limit

- Make smaller payments throughout the month to keep your balance low

Suppose you're on a tight budget, aim to keep your current balance under 30% of your available credit. This helps maintain healthy credit utilization and keeps your credit score steady.

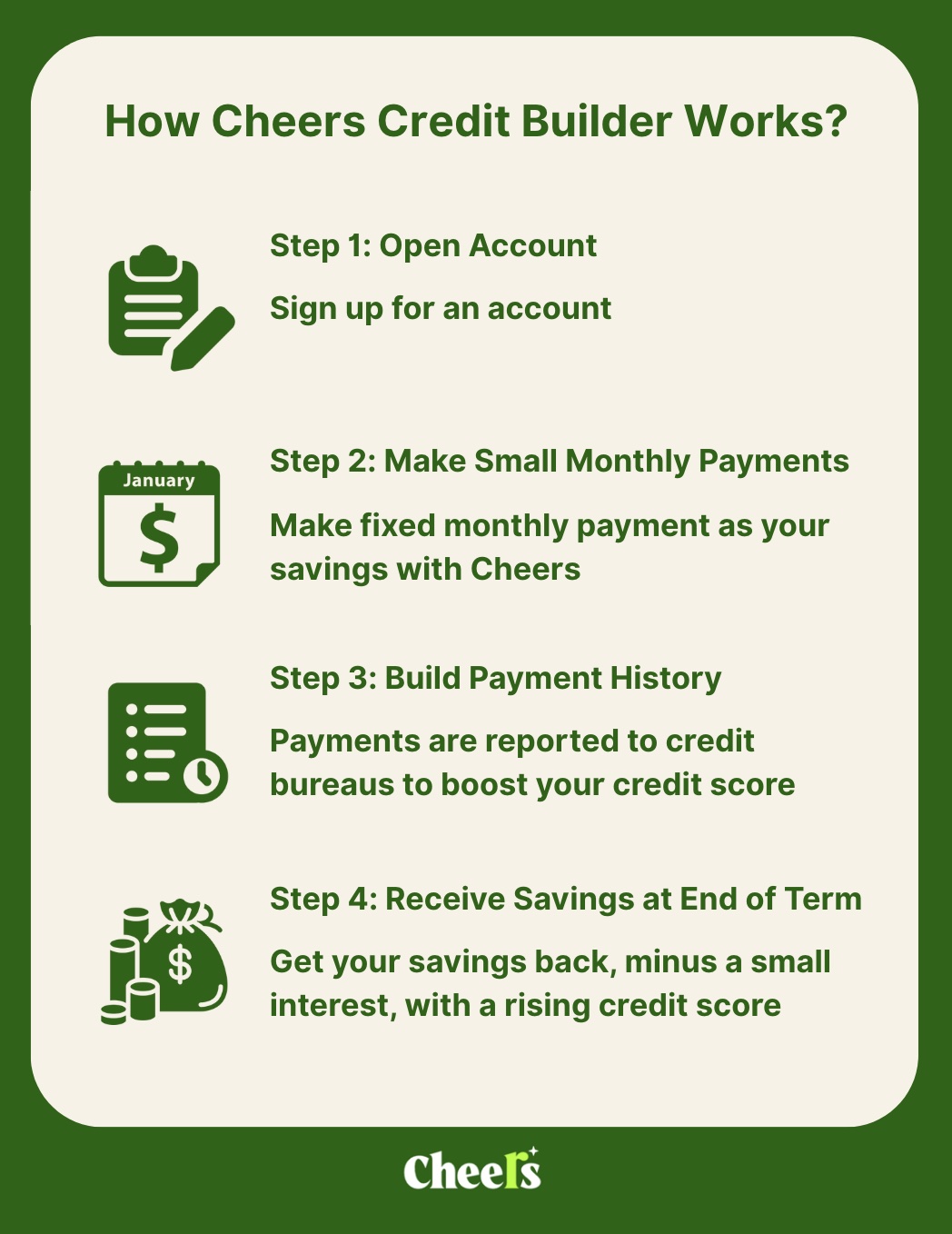

Cheers Helps You Build Credit While You Save

If you’re working to improve your credit or just starting out, managing your current balance is part of the equation. But building credit can take more than good habits—it also requires reporting.

Cheers Credit Builder makes it easier to grow your credit without needing a credit card. When you open a Cheers account, your payments get reported to all three major credit bureaus each month. There’s no hard credit check, no setup fees, and no membership charges. You select a monthly plan, make fixed payments, and at the end of your term, you get your savings back minus interest.

With Cheers, you can start building a payment history from day one—something that can take longer with other credit builder loans. Learn more and get started in just a few minutes at cheers.credit.

References: