Author: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 5/24/2025

Table of Contents

- Why My Friend Linda Wanted Out

- How to Get Out of a Car Loan Without Wrecking Your Finances

- Selling or Trading In: What You Need to Know

- Repossession Isn’t Just Giving Up

- Can You Refinance or Transfer the Loan?

- If You’re Upside Down on the Loan

- Rebuilding Credit After a Tough Decision

Why My Friend Linda Wanted Out

My friend Linda financed her first car right after college. The payments felt manageable at first, but a year later, everything changed. Rent went up, her job hours were cut, and suddenly, her $450 car payment no longer made sense. She asked me, “Do you know how to get out of a car loan without destroying your credit?”

Her story is familiar. Many people are in the same spot — locked into a loan that no longer fits their budget. Luckily, some options don’t involve wrecking your credit or draining your savings.

How to Get Out of a Car Loan Without Wrecking Your Finances

The first step is understanding your current loan. Review your payoff balance, the current value of your car, and whether there are penalties for paying it off early. You can usually find this info on your loan statement or by calling your lender directly.

Then comes the question: what’s the smartest way to exit? According to the Consumer Financial Protection Bureau, understanding the terms of your loan is key to avoiding long-term damage.

If your payments are too high or the car isn’t worth what you owe, you're not alone. Linda learned this quickly and started exploring her choices.

Selling or Trading In: What You Need to Know

Selling your car privately or trading it in are two common ways people get out of a car loan. Linda used Kelley Blue Book to check the value of her car. It turned out her car was worth more than her loan balance — a lucky break. She sold it, paid off the loan, and used the extra cash to purchase a more affordable used car.

If your car is worth less than the loan balance, this is called being “upside down.” You’d need to cover the difference with cash or roll it into a new loan, which isn't ideal if you're trying to cut costs.

Sites like NerdWallet break down the pros and cons of both options clearly, especially if you're deciding whether to sell or trade.

Repossession Isn’t Just Giving Up

Some people consider returning the car to the lender. This is called voluntary repossession. While it may sound like a clean break, it still negatively impacts your credit. According to Experian, a repossession — voluntary or not — can stay on your credit report for seven years.

Linda considered this but realized the long-term damage wasn’t worth it. If you’re facing this decision, it might be worth calling your lender first. Some offer hardship programs, deferments, or revised payment plans.

Can You Refinance or Transfer the Loan?

If your credit has improved since taking out the loan, refinancing could be a smart move. It means replacing your current loan with a new one, often with a lower interest rate or longer term. This can reduce your monthly payments and give you some breathing room.

Some lenders also allow loan transfers. This means someone else takes over your loan — but not all lenders offer this, and the new borrower usually needs good credit. It’s worth asking about if you have someone willing to step in.

Linda didn’t qualify for refinancing, but if you’re in a better spot credit-wise, Bankrate offers a clear guide on how it works.

If You’re Upside Down on the Loan

Being “upside down” on a car loan means you owe more than the car is worth. If this sounds familiar, you have a few options. You can keep the car and pay down the loan until it matches the car’s value. You can try to sell and cover the difference with savings. Or you can refinance to reduce your monthly cost and avoid falling further behind.

Linda was lucky she wasn’t underwater, but many people are. Staying in the loan and making extra payments to catch up may take time but can save your credit in the long run.

Rebuilding Credit After a Tough Decision

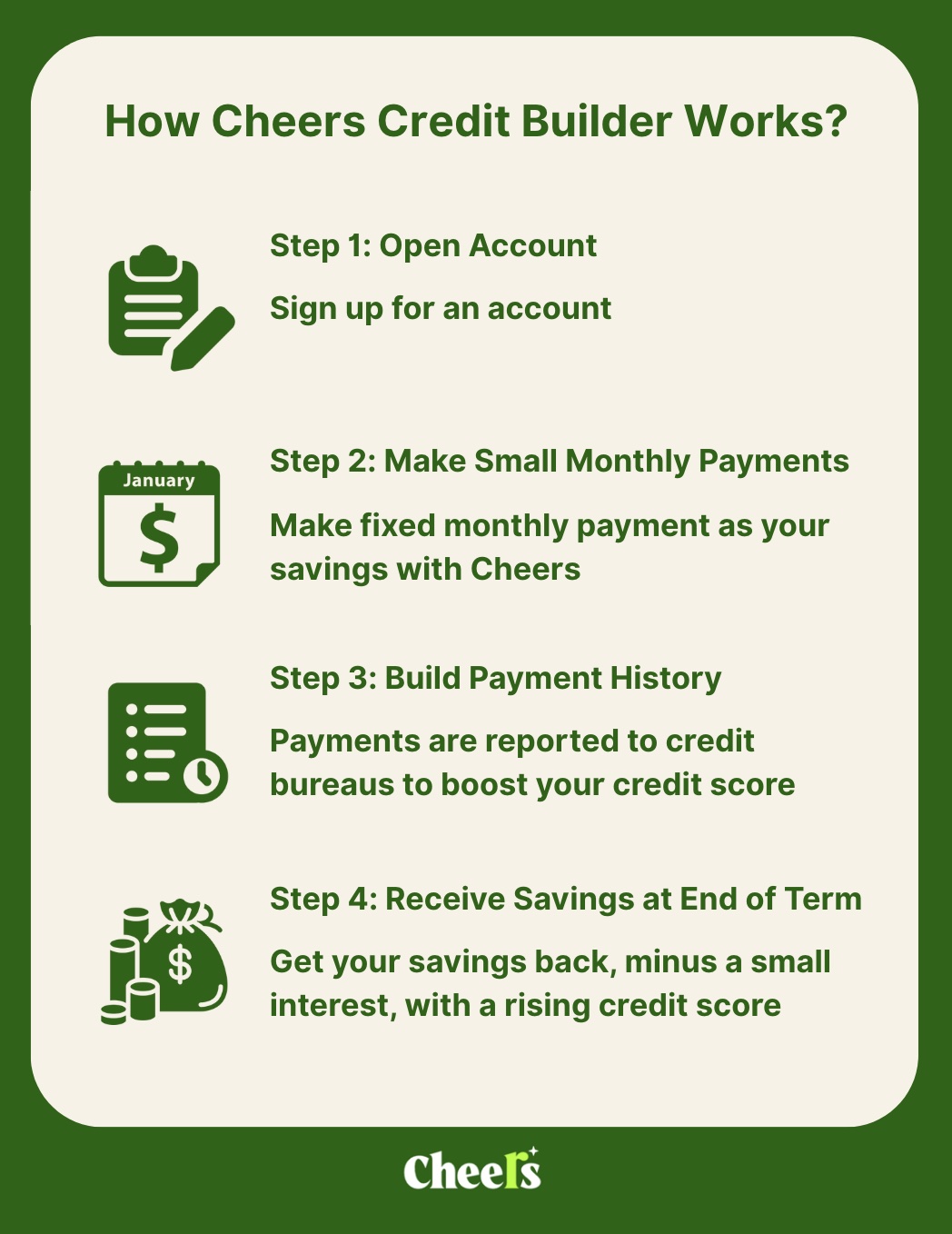

If exiting your loan damaged your credit or left you with fewer options, don’t panic. Rebuilding is possible. One of the easiest ways is with a credit builder loan, like the one offered by Cheers.

Cheers helps people rebuild credit by reporting monthly payments to all three major credit bureaus. There’s no credit check, no setup fee, and your payments are saved in an FDIC-insured account. When the loan term ends, you get your savings back, minus interest. This method helped Linda start repairing her score right away after she sold her car.

Getting out of a car loan can be tough, but it’s not the end of the road. Like Linda, you just need the right plan and the right tools to move forward.

References: