By: Aimee Cheng (Plant mom, dog lover, and passionate advocate for financial independence)

Date: 5/3/2025

Table of Contents

- Why Credit Building Matters

- How Credit Cards Help Build Credit

- Keep Your Balance Low

- Never Miss a Payment

- Be Careful With New Accounts

- Building Credit Without a Credit Card

- How Cheers Credit Builder Can Help

Why Credit Building Matters

If you’re trying to build credit, you’re not alone. Over 45 million Americans have little to no credit history. This can make it hard to qualify for an apartment, get approved for a car loan, or even pass a job background check. For many, the best way to use a credit card to build credit starts with small, consistent habits. Used the right way, credit cards can help you grow your score and open doors to better financial opportunities.

Many people turn to credit cards as a way to get started. Used right, they can help build credit quickly. Used wrong, they can hurt your score or put you in debt. That’s why understanding the best way to use a credit card to build credit is key.

How Credit Cards Help Build Credit

According to the Consumer Financial Protection Bureau, Credit cards can influence your credit score through several factors, but two of them matter the most:

- Payment history (35% of your score): Are you making your payments on time?

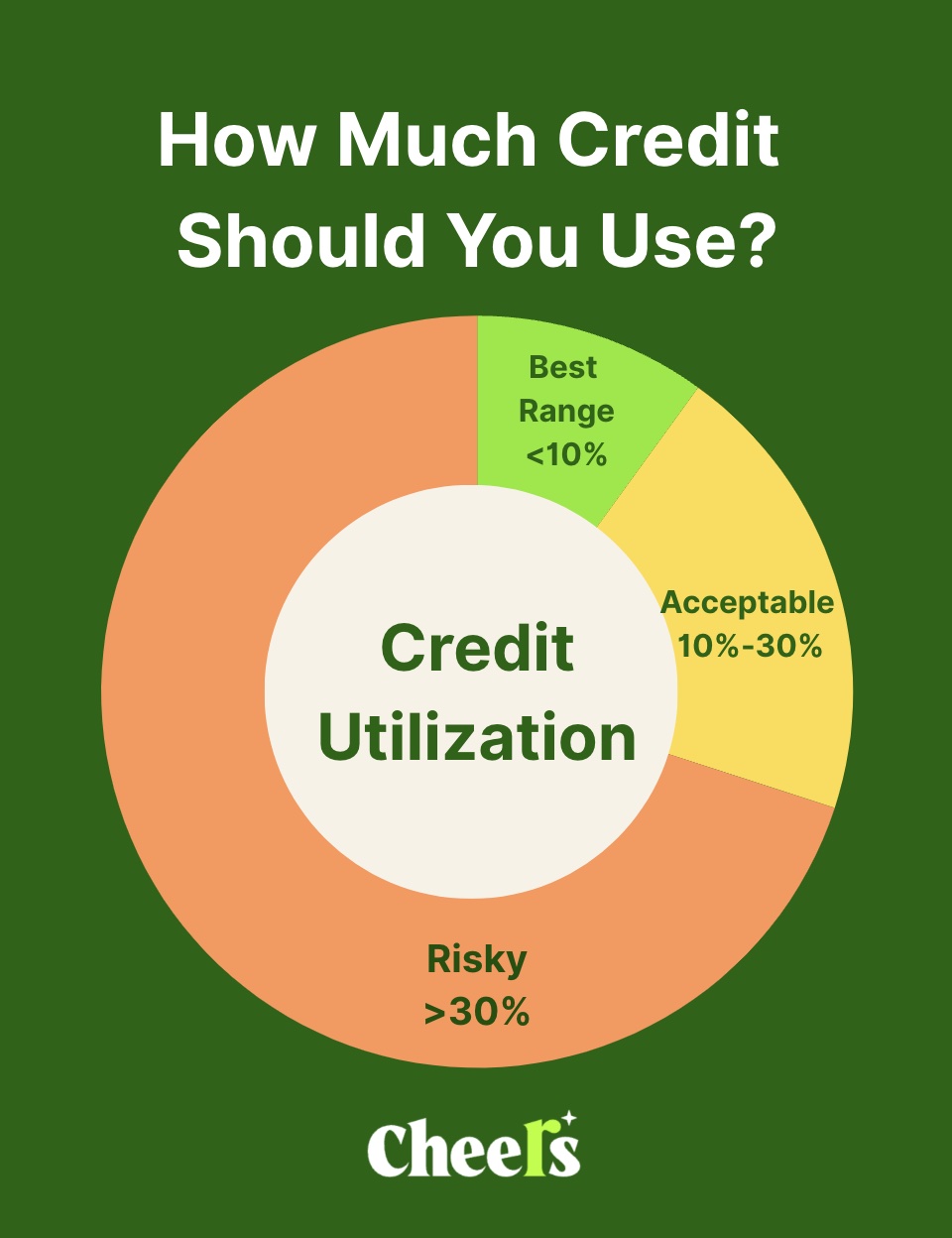

- Credit utilization (30%): How much of your available credit are you using?

Lenders want to see that you can borrow money and pay it back responsibly. Your credit card activity gives them this picture.

Keep Your Balance Low

One of the best ways to use a credit card to build credit is to keep your usage low. This means using less than 30% of your available credit. If you can keep it under 10%, even better.

Let’s say you have a $500 credit limit. Try to keep your balance under $150. Better yet, aim for under $50 if possible. You don’t need to carry a balance from month to month — just make small purchases and pay them off. This shows lenders you can use credit wisely without relying on it too heavily.

Never Miss a Payment

Paying your credit card bill on time is the most powerful thing you can do to build credit. Even one late payment can hurt your score and stay on your report for years.

To avoid this, set up automatic payments or add a reminder to your calendar. You don’t have to pay interest or carry a balance — just pay at least the minimum on time each month. If possible, pay the full amount to avoid interest altogether.

On-time payments build your score. Late ones set you back.

Be Careful With New Accounts

Opening a new credit card can increase your available credit, which may help your utilization ratio. But applying for too many cards at once can backfire. Every application triggers a “hard inquiry”, which can lower your score temporarily.

Stick to one or two cards at first. Use them for everyday expenses, pay them off, and let your score grow over time. You don’t need five cards to prove you’re responsible — just good habits.

Building Credit Without a Credit Card

Not everyone can get approved for a credit card, especially if you’re just starting out or rebuilding after a setback. That doesn’t mean you’re stuck.

Credit builder loans offer another way to grow your score. These are small loans where your monthly payments are reported to credit bureaus. You don’t get the money upfront — instead, you’re saving while building credit.

Tools like this are especially helpful if you want to avoid the temptation of credit cards or just need a safer option.

How Cheers Credit Builder Can Help

Cheers Credit Builder is a simple way to build credit — without needing a credit card. You choose a plan between $528 and $3,168 and make monthly payments for 12 to 24 months. Each payment is reported to all three major credit bureaus: Experian, Equifax, and TransUnion.

There are no setup or membership fees, just a flat 1% monthly APR. Your payments are saved in an FDIC-insured account through Cheers’ partner banks. At the end of the loan, you get your money back, minus the interest.

- No credit check

- No surprises

- Start building your payment history on Day 1

Cheers isn’t a bank. Deposit accounts are held by partner banks, Member FDIC. But the credit growth is real — and so are the savings.

Learn more at Cheers.Credit.